Tour News

Reserve Cup returns to Marbella: padel's private tour finds its formula

Aleksandr Malkov17 Jun 2026

Every padel investment deck quotes a sub-24-month break-even. We built the model and found the number is real, just for a market that no longer exists.

Every padel investment deck has the same slide: a utilization curve pointing up and to the right, a €/hour rate that never erodes, and a headline promising payback in 18–24 months. Court manufacturers repeat it, club consultants repeat it, and now the general business press repeats it while covering the sport's growth. The €6 billion market projection that anchors most of this coverage traces back to the Playtomic Global Padel Report, the industry's reference dataset, which we'll come back to. The payback claim has a source too.

It came from 2021.

Start with capex, because that's where the myth begins. The court itself is the cheap part: a quality panoramic court runs €22,000–35,000 supplied, and foundations and screed add another €10,000–15,000. Stop counting there and padel looks like a vending machine, which is exactly how the decks present it.

For an indoor operation the building is the real line item: a steel or tensile structure for a four-court block alone runs €120,000–250,000, before locker rooms, reception, ventilation and a bar. Turnkey new-build estimates from court suppliers themselves now sit at €70,000–90,000 per court all-in. UK projects are quoting £45,000–80,000 per court, and that's before London-grade site costs.

So what does the often-quoted "€600k for a 5–7 court park" actually buy? One specific thing: a leased warehouse retrofit. Existing shell, ceiling height of at least six meters, landlord-funded basics, courts and fit-out on your balance sheet. That works out to roughly €85,000–120,000 per court fully loaded, and it's the only configuration where €600k is honest. A ground-up build for the same court count is a €1.5–2.5M project. Half the payback claims you'll read quietly compare a retrofit's capex against a new-build's revenue fantasy.

One genuine economy worth knowing: building courts in batches cuts per-court cost by 15–30% through shared groundwork and bulk components. This is why sub-4-court urban clubs almost never pencil. They carry full fixed costs on a revenue base that can't absorb them.

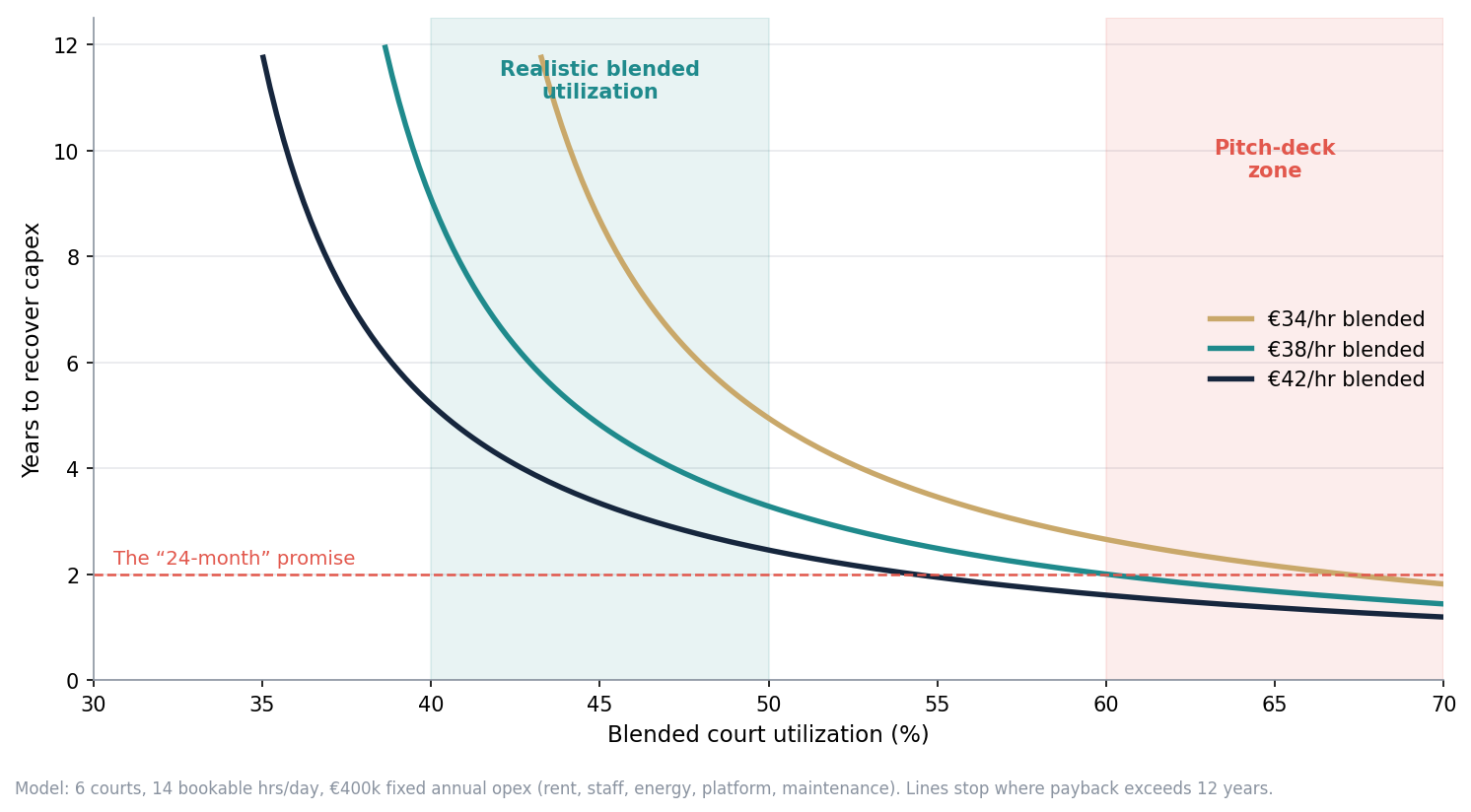

Take the favorable case: six courts, leased warehouse, €600,000 in.

Six courts open fourteen bookable hours a day gives you roughly 30,700 court-hours a year. Now the assumption that decides everything: how many of those hours you actually sell. Decks assume 60–70%. Reality in a competitive European market is a blended 40–50%. Evenings and weekends sell out. Tuesday at 11:00 does not care about your Instagram. At 45% utilization and a blended €38/hour (peak at €45–50, off-peak discounted, league and coaching blocks in between), court rental brings in about €520,000.

Most of that disappears into the cost stack. Rent on 1,800–2,200 m² of urban-adjacent warehouse takes €120,000–220,000 depending on the market, and rent, not energy or staff, is the line that kills clubs. Lean staffing of two to three FTE plus part-time coaching admin: €90,000–130,000. Energy for a lit, ventilated indoor hall: €40,000–80,000, a number Scandinavian operators will reappear to comment on shortly. Platform fees, insurance, maintenance, turf reserve and marketing: another €50,000–70,000.

What's left is EBITDA of roughly €80,000–180,000. Against €600,000 invested, payback lands between 3.5 and 7 years. A well-run club in a healthy catchment sits around four to five. For bricks-and-mortar leisure that's a genuinely good return, better than most gym formats. It's also not 24 months.

So when is 24 months real? Run the same model at 65% utilization with zero price pressure and cheap rent. EBITDA jumps past €300,000 and the deck math works. Those conditions describe exactly one situation: a first mover in an undersupplied market during a demand spike. Pandemic-era Sweden. Early Dubai. Maybe your city, for about eighteen months, until your payback slide raises the money that builds your competitors.

That's the structural joke at the heart of padel economics: the 24-month number is self-destroying. Returns that good attract capital, capital builds courts, courts compete away the returns. The payback pitch is the mechanism of its own collapse.

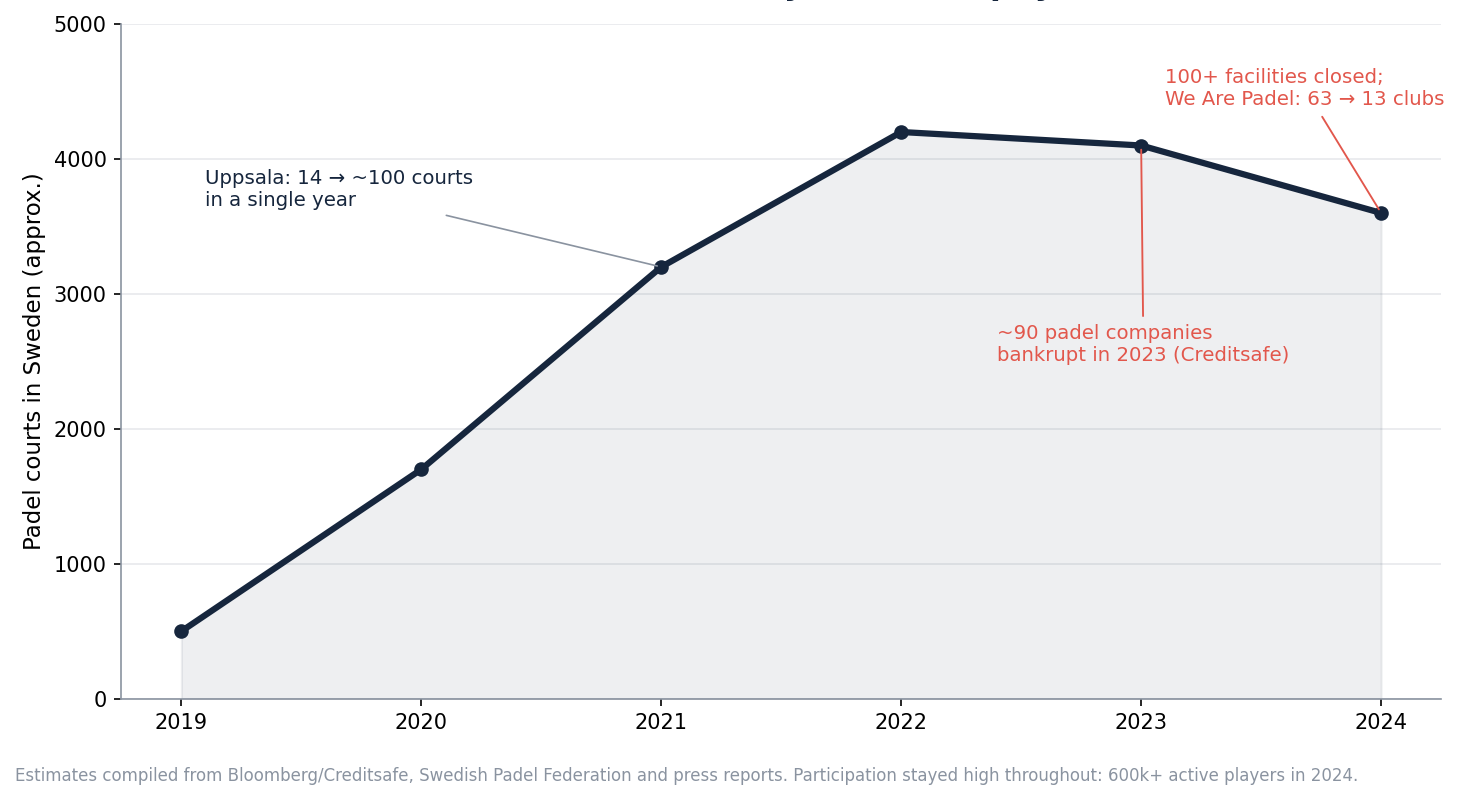

Between 2019 and 2022, Sweden went from a few hundred courts to over 4,200, more building than anywhere outside Spain. Uppsala, a city of 200,000, went from 14 courts to nearly 100 in a single year. Private equity treated padel as industrial real-estate arbitrage: cheap suburban sheds, a low-friction sport, pandemic demand that looked structural.

By the end of 2024 the tally read: more than 100 facilities closed, roughly 90 padel companies bankrupt in 2023 alone according to Creditsafe data reported by Bloomberg, Triton-backed We Are Padel down from 63 Swedish clubs to 13, PDL Group rescued with €24M, and industry estimates of capital destroyed approaching €500 million. Occupancy at some venues fell from pandemic peaks of 80–90% to single digits. Former padel halls now operate as discount supermarkets.

The detail everyone misses: demand never collapsed. Over 600,000 Swedes were still playing in early 2024, per capita still among the highest participation in Europe. The bust was pure supply-side: too many courts, financed on 65%-utilization math, hit simultaneously by 5x energy prices and by each other. Every operator's deck was individually plausible. Collectively they were impossible.

The survivors share one trait, and it isn't location. The clubs that lived converted bookings into belonging: coaching programs, junior pathways, leagues, social play. An empty shed with glass walls competes on price until it dies. A club with a coaching pipeline and a Thursday league has switching costs.

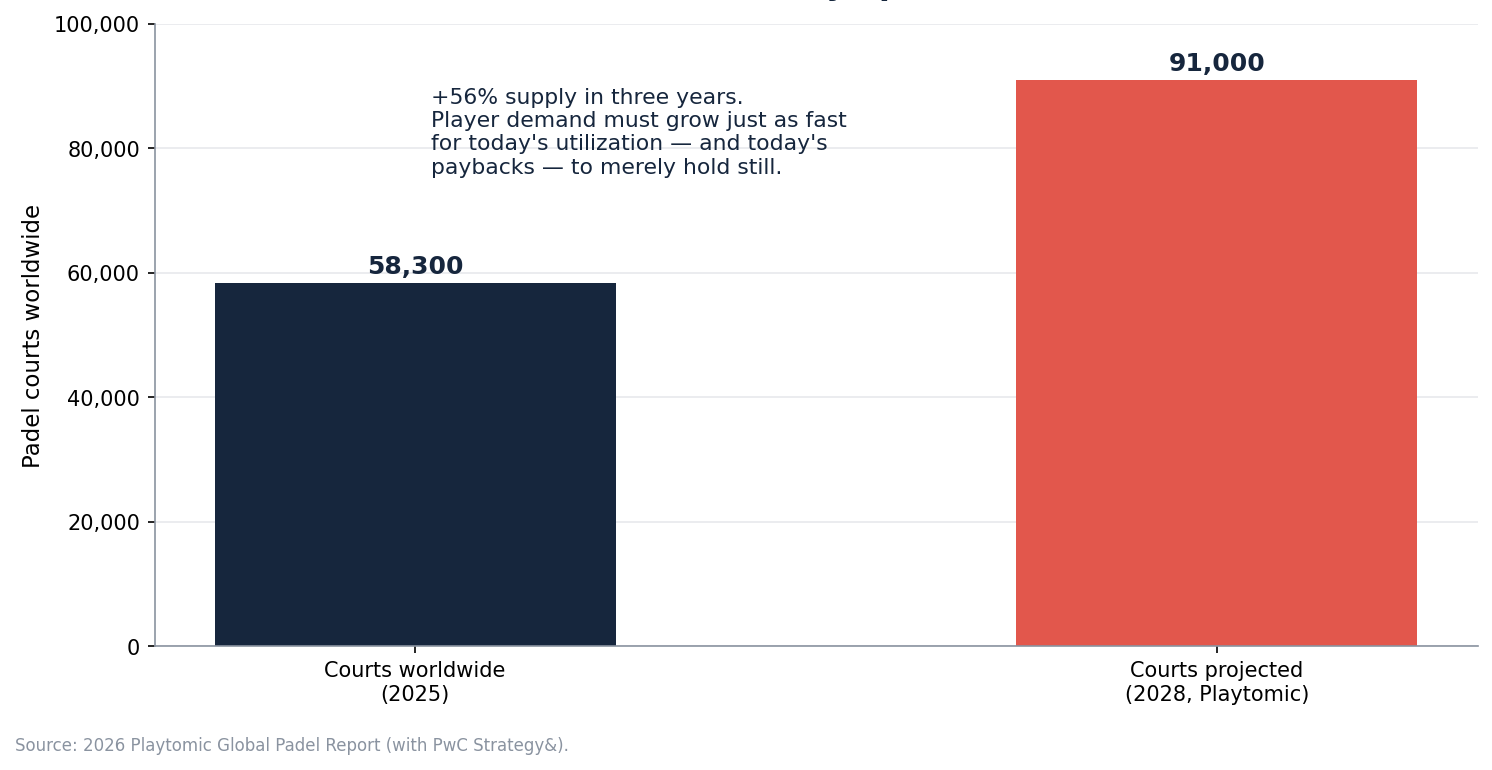

The 2026 Playtomic Global Padel Report, produced with PwC's Strategy&, is the dataset everyone in this industry quotes, us included. The headline figures: 20,900+ clubs, 58,300 courts and 19.4 million players worldwide, with nearly 5,000 new clubs and 8,000 new courts added in 2025 alone, and a forecast of 91,000 courts by 2028. It's the best census the sport has, and this year's edition declares padel is becoming "a recognised investment category" and "a real estate asset class." Read it, then apply three corrections.

The archetype trap. The report's new framework classifies the UK and Germany as "Hotspot" markets, defined by demand consistently outpacing supply and strong unit economics attracting institutional capital. Every word of that description fit Sweden in 2020. An archetype is a snapshot of today's supply-demand balance; the risk lives in the pipeline, which the snapshot doesn't capture. In one London borough alone, five padel developments are currently moving through planning, and none of the applications includes a demand assessment. A "Hotspot" label on the cover of an industry report is precisely how a pipeline like that gets financed.

The 91,000-court arithmetic. Going from 58,300 to 91,000 courts means 56% more supply in three years. For today's utilization rates, and therefore today's paybacks, to merely hold still, player demand has to grow just as fast. It might. But note that supply is countable and demand isn't: the report says 19.4 million players, while federation materials have circulated figures north of 30 million. When an industry can count its courts precisely and only estimate its players, it reliably over-builds the thing it can count.

The incentive question. Playtomic is a booking marketplace. Its revenue grows with the number of courts on the platform whether or not the operators of those courts ever recover their capex. Oversupply means more inventory and sharper price competition, which is painful for clubs and largely fine for the aggregator. None of this makes the data wrong, and the report deserves its "Bible" status as a census. But its framing of padel as a real estate asset class should be read for what it is, and with the awareness that "industrial real-estate arbitrage" was, word for word, the thesis Swedish private equity lost €500 million on.

To be fair, the report contains its own quiet warning. Its wellness section finds that nine out of ten leading clubs already generate revenue off the court. The most bullish document in padel agrees, between the lines, with the central lesson of the Swedish bust: pure court rental is not a business anymore.

If you're building, operating or financing a club, replace the payback slide with five questions.

Catchment, not country. National growth statistics are irrelevant to your P&L. What matters: active players within a 15-minute drive, divided by competing courts in the same radius, plus the courts in the planning pipeline, which is public information almost nobody pulls.

Stress-test at 35% and minus 20%. Run the model at 35% blended utilization and a 20% price cut, the conditions eighteen months after two competitors open. If the club survives that, build it. If it only works at 60%, you're not buying a business, you're buying a window.

Rent sets your floor. Negotiate lease length, break clauses and ideally turnover-linked components. Swedish operators on fixed long leases at boom-era rents had no way down. A building you don't own can still bankrupt you.

Secondary revenue is the moat. Court rental should be 70% of revenue or less at maturity. Coaching, academies, leagues, corporate and F&B are higher-margin and defensible. As Sweden showed, they were the difference between the 13 clubs that survived and the 50 that didn't.

Energy is a position, not a cost line. Indoor padel in a cold climate is an energy-intensive real-estate business. Hedge it, solar it, or model it at double. Scandinavian operators learned this at five times.

Padel club economics are good. Run well, in a sane catchment, on a defensible lease, a club returns its capital in four to six years and compounds from there, a better risk-adjusted profile than most of the leisure sector. The sport doesn't need the 24-month myth. The only people who need it are the ones selling you the build.

Vamos advises on club development and court construction, which means our incentive is that your club is still open in year five. If you're underwriting a padel project and want the model behind this piece, write to us.